James Sanson

Founder, Listing Specialist

23+ years in Maricopa real estate. 1,000+ closings. Specializes in seller representation and complex transactions.

Founder, Listing Specialist

23+ years in Maricopa real estate. 1,000+ closings. Specializes in seller representation and complex transactions.

Maricopa, AZ, closing costs explained for sellers and buyers. Line by line, with current 2026 numbers.

Real Broker LLC · Licensed in Arizona

Updated July 2026

By James Sanson, REALTOR®. Licensed Arizona real estate agent since August 2002. Maricopa specialist since 2004. 1,000+ closings across new construction, resale, and distressed-property transactions. See about James Sanson and the team.

Published 2026-05-20. Last reviewed 2026-05-20.

Quick answer

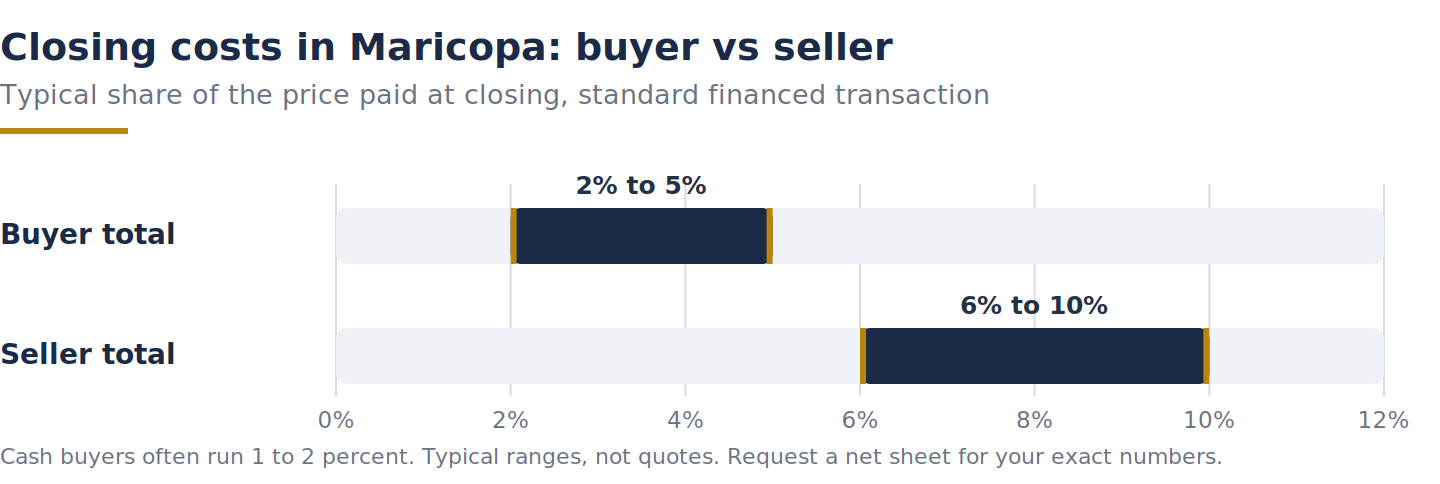

Buyer closing costs in Maricopa, AZ, typically run 2 to 5 percent of the purchase price. Seller closing costs typically run 6 to 10 percent, with the real estate commission as the largest single item. Exact figures depend on price, loan program, title company, HOA, and contract terms. Ask your lender for a Loan Estimate and your title company for a net sheet to see your actual numbers, and call 520-838-8037 for a Maricopa-specific walkthrough.

On this page

If you are buying or selling a home in Maricopa, AZ, closing costs are the line items beyond the purchase price that settle the transaction. Some are loan fees. Some are title and escrow fees. Some are prorations of taxes, HOA dues, and insurance. Some are county recording fees. This page covers what each side typically pays in a Maricopa transaction, where Arizona customs differ from those in other states, and how to estimate your own numbers before you go under contract.

Closing costs are real money. On a 425,000-dollar Maricopa home, buyer closing costs of 3 percent are roughly 12,750 dollars, and seller costs of 8 percent are roughly 34,000 dollars. Knowing these ranges before you write or accept an offer prevents surprises at the closing table.

This page is informational. Specific tax treatment, deductibility, and legal allocation of costs depend on your situation and on the terms of your purchase contract. For tax questions, consult a CPA or qualified tax professional. For contract or title questions, consult an Arizona-licensed attorney.

In a typical Maricopa, AZ sale, buyers pay about 2 to 5 percent of the price in closing costs, and sellers pay about 6 to 10 percent. These are typical ranges, not quotes. Call 520-838-8037 for a net sheet.

The following ranges reflect typical Maricopa, AZ transactions as of publication. Your actual costs may run higher or lower depending on the variables noted in each section below.

These are ranges, not promises. Reach out for a current-market net sheet tailored to your specific Maricopa address and price point.

| Closing cost | Buyer | Seller |

|---|---|---|

| Loan and lender fees | Yes | No |

| Appraisal | Yes | No |

| Prepaids and escrow reserves | Yes | No |

| Lender title insurance policy | If financing | No |

| Owner title insurance policy | No | Often in Arizona |

| Escrow and settlement fee | Often split | Often split |

| County recording fees | Deed recording | Payoff recording |

| Property tax and HOA prorations | Prorated | Prorated |

| HOA transfer and capital fees | Varies | Varies |

| Real estate commission | No | Negotiable |

Buyer closing costs in Maricopa fall into four categories: loan costs, title and escrow costs, prepaid items and reserves, and miscellaneous fees.

Loan costs (paid to the lender):

Title and escrow costs (paid to the title company):

Prepaid items and reserves (held by the lender for future bills):

Miscellaneous:

Seller closing costs are dominated by the real estate commission, but several other items add up. Here is the typical breakdown for a Maricopa, AZ sale.

Net proceeds are what remain after all of the above are deducted from the sale price and the existing mortgage payoff. Request a seller's net sheet early in the listing process so you know your bottom line before the first offer comes in.

Two title policies are typically issued in a Maricopa, AZ purchase. The lender's policy protects the mortgage company against ownership claims, liens, and recording errors that could affect the loan. The owner's policy protects the buyer against the same risks, for as long as the buyer owns the home.

By Maricopa-area custom, the buyer pays for the lender's policy, and the seller pays for the owner's policy. The purchase contract can change this allocation in either direction, and in competitive market cycles, buyers sometimes offer to pay for the owner's policy to make their offer more attractive to the seller.

Both policies are one-time premiums paid at closing. There are no monthly payments and no renewals. Premiums are filed with the Arizona Department of Insurance and Financial Institutions and are generally similar across title companies, though some companies offer reissue discounts when a recent prior policy exists on the property.

Property taxes in Pinal County are billed in arrears in two installments each year. The first half covers January through June and is due October 1 (delinquent after November 1). The second half covers July through December and is due March 1 (delinquent after May 1).

Because taxes are billed after the period they cover, the seller has been living in the home and accruing tax liability for some number of days before closing without yet receiving a bill. At closing, the title company calculates the number of days the seller owned the home during the current tax period and credits the buyer with the seller's share of taxes. The buyer then pays the actual tax bill when it comes due.

A typical Maricopa, AZ, single-family home pays roughly $1,200 to $2,800 per year in property taxes, depending on the assessed value, district, and any voter-approved overrides. Your title company's net sheet will show the exact proration based on the closing date. For tax questions specific to your situation, including any homeowner exemptions you may qualify for, consult a CPA or the Pinal County Assessor's office.

Most established Maricopa subdivisions have an HOA, and HOA-related fees are paid by both the buyer and seller at closing.

HOA documents are delivered to the buyer during escrow. Review them before contingencies expire so you have a clear picture of monthly dues, any special assessments, and the rules that govern the community. For neighborhood-specific HOA structures, see our pages on Maricopa neighborhoods when you are comparing communities.

Loan-related costs are the largest single category of buyer closing costs after the down payment. The specific items and amounts depend on the loan program.

Conventional loans. Typically, the lowest closing costs among standard programs. Lender fees are limited to origination, underwriting, processing, and credit report. Private mortgage insurance applies if the down payment is under 20 percent, and the first month's payment is collected at closing.

FHA loans. Include an upfront mortgage insurance premium of 1.75 percent of the loan amount, financed into the loan rather than paid at closing in cash. Monthly mortgage insurance also applies. FHA closing costs tend to be slightly higher than conventional because of the upfront premium and the additional documentation.

VA loans. Include a one-time VA funding fee that varies by service category and down payment, and is typically financed into the loan. Eligible disabled veterans are often exempt from the funding fee. VA loans also restrict which closing costs the buyer can pay, so the seller may carry items the buyer would otherwise pay.

USDA Rural Development loans. Available for qualifying properties at the edges of Maricopa. Include an upfront guarantee fee and an annual fee paid monthly. Income and property eligibility apply.

Your lender will provide a Loan Estimate within three business days of your application. Compare Loan Estimates from at least two lenders before committing. Differences in lender fees and rate structure can move your closing costs by several thousand dollars on a typical Maricopa purchase.

Several legitimate strategies reduce closing costs for buyers and sellers in Maricopa.

Buyer strategies:

Seller strategies:

You can produce a reliable closing cost estimate before going under contract. Here is the order of operations.

If you are early in the process and just want a ballpark figure, call 520-838-8037, and we can run quick numbers for any Maricopa, AZ price point.

Closing costs are easier to navigate with someone who has worked through hundreds of Maricopa transactions and knows the local title companies, HOAs, and contract conventions. Whether you are buying with a Maricopa buyer agent or selling with a Maricopa listing agent, call The James Sanson Team if any of these apply.

Important. This page is informational, not tax or legal advice. Closing cost allocations, loan program rules, and tax treatment can change, and the figures above reflect typical ranges for Maricopa, AZ, as of publication. Confirm specific amounts with your lender, title company, and CPA. The James Sanson Team is not a tax advisor or attorney. For your specific situation, consult a CPA or an Arizona-licensed attorney. Call 520-838-8037 to talk through your transaction with a Maricopa specialist.

If you are buying or selling in Maricopa, AZ, and want a clear picture of closing costs before you sign anything, call 520-838-8037 to talk with a Maricopa-area real estate agent with over 23 years of Arizona licensure and 1,000+ closings.

Tell us about your situation. We will connect you with whichever team member fits best. No pressure, no spam, just real help.

Whether you're buying, selling, or just exploring, call us. No obligation.

520-838-8037James Sanson | Real Broker LLC | Licensed in Arizona

Call 520-838-8037 right now, or fill out the form and we will reach out within one business day.